The shocking rise of mortgage costs since Iran war – and when they might go down again

.jpeg?width=1200&height=800&crop=1200%3A800&ssl=1 "The shocking rise of mortgage costs since Iran war – and when they might go down again")

The Middle East conflict has had a string of knock-on effects in the UK, including for homeowners who are now facing higher bills.

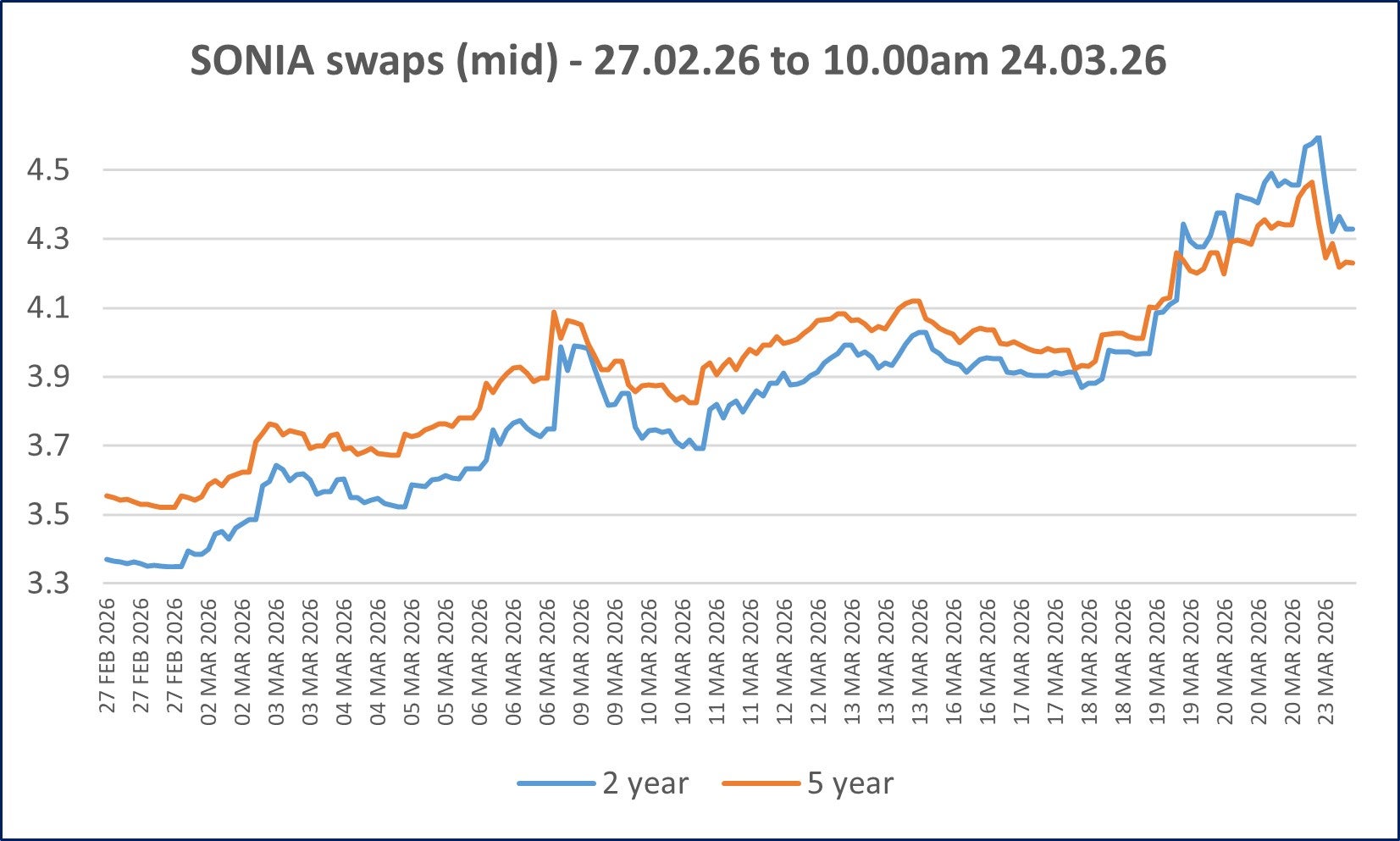

Those who were closing in on a new house purchase, or renewing their deals on current property, would have been hoping for an interest rates cut by the Bank of England (BoE) in March or April, as was widely expected. Instead, a hold for now is on the cards – and swap rates, which mortgage deals are actually priced on, have soared.

The Independent has been shown data comparing the best rates on offer from one major high street bank on 27 February, the day before the war started, to their best rate on offer today. The difference highlights the rapid rise – and the associated extra cost – for homeowners.

For a two-year fix, it has gone from 3.67 per cent to 4.37 per cent. Assuming a £250,000 mortgage value on a 25-year term, that’s a difference of more than £96 a month, or £1,160 extra per year, if you were eligible for the original deal but waited until now – just 26 days ago.

On a five-year fix, the best deal has moved from 3.89 per cent to 4.54 per cent, equating to £90 a month or £1,089 per year more in the same scenario.

A Barclays Property Insights Report for this month showed that 1 per cent of mortgage holders said their deal is expiring within the next four weeks, rising to 8 per cent within the next three months.

Swap rates vs interest rates

It’s important to know why mortgage rates have increased (or could change upwards or downwards again) when the BoE hasn’t budged.

The BoE sets what’s termed as the bank rate, or base rate – or just “the interest rate” to most. That’s 3.75 per cent right now.

Get a free fractional share worth up to £100.

Capital at risk.

Terms and conditions apply.

Go to website

ADVERTISEMENT

Get a free fractional share worth up to £100.

Capital at risk.

Terms and conditions apply.

Go to website

ADVERTISEMENT

However, that’s just as the name implies: the base from which other markets move from. For mortgages, swap rates are the driving force behind pricing the interest rates you’ll see on each product available from lenders.

Swap rates are essentially a type of contract which is traded based on expectations of where money markets think rates will move in future. So, if a bank or building society is buying these at a higher price, that’s their wholesale cost for the money which they will lend you as a fixed-term mortgage holder – and so they will charge slightly above that rate within the mortgage product. When swap rates come down, the money is “cheaper” and mortgage deals can likewise fall again.

To put that into context, swap deals were trading well below 4 per cent and so there were lots of sub-4 per cent mortgage deals on the market for people to choose from. As swap rates shot up, lenders removed those deals and replaced them with higher-rate offers.

“Since the start of the Iran war, swap rates have risen by more than a full percentage point. In response, the price of fixed-rate mortgages has spiked by similar or even higher amounts,” Peter Stimson, director of mortgages at MQube, told The Independent.

“Intense volatility on the swaps market has led several smaller lenders to temporarily withdraw their fixed rate offerings until they can be certain where the market will settle.

“Given the huge spike in fixed rate pricing – which will hopefully be temporary – many mortgage brokers are now looking to switch new clients onto tracker products in the shorter term. Most tracker mortgages have no early repayment charges, so borrowers who take out a tracker in the coming weeks could switch easily to a fixed rate loan when rates improve.”

What happens next

With the UK economy struggling, the BoE would have been hoping to cut interest rates further to stimulate businesses into spending money. That can lead to lowering the unemployment rate – which has risen to 5 per cent – as well as higher consumer spending and less cost pressures for companies.

However, rising inflation is a barrier to doing that. Although Wednesday’s report showed February inflation sticking at 3 per cent, that’s very much a rear-view mirror look when we already know rising costs through fuel, energy bills and production are all coming as a result of oil prices rising due to Iran closing the Strait of Hormuz.

“There’s a summer 1939 feel to this inflation data. Everyone knows something very bad is about to happen, we just don’t know how bad it will be yet,” Samuel Fuller, director of Financial Markets Online, said. “The first strikes on Iran were launched on the last day of February. The inflationary picture at that point was largely benign.

“The Bank of England has torn up last month’s inflation forecasts and we wait to see whether the coming weeks will bring inflationary headwinds or a hurricane.

“So while rising inflation isn’t yet showing on the UK’s economic dashboard, there are plenty of warning lights already glowing red and all this has created a genuine risk of stagflation.”

.jpeg)

This is relevant because the property market is a big contributor to the overall UK economic picture and when mortgages are more expensive, some buyers are more reluctant to push through a move, preferring instead to wait and see if rates come down once more.

That brings the question of, with Donald Trump presenting a peace plan which Iran seems to be rejecting outright, when swap rates might start to edge back towards 4 per cent or below once more.

“There are two possible scenarios for mortgages next. The first and best is that there is a peace deal soon, and things recover some kind of normality. While swap rates should quickly drop back below 4 per cent, it may take quite a few months before we see mortgage rates falling back to the levels we saw in February,” said Mr Stimson.

“The second and far less positive scenario is that the war drags on for months, with the Straits of Hormuz staying closed.

“Interest rate markets are largely pricing for this now, so whilst further rate rises may be limited, this scenario would make borrowing very challenging, adding a significant drag to the whole UK economy and raising the spectre of stagflation.”